Splitting Renters Insurance Fairly: A Guide for Roommates

Author

Date Published

Imagine you come home to find your apartment ablaze, smoke billowing from the windows, and your personal belongings destroyed. Sounds like a nightmare, right? With renters insurance, this catastrophe turns into a manageable setback. And the best part? It doesn't have to break the bank, especially when shared with your roommates.

This guide is your roommate cost-sharing cheat sheet for conquesting renters insurance costs without the hassle. We'll cover everything you need to know, from the basics of renters insurance to navigating tricky conversations and ultimately finding the fairest way to split the bill. Let's jump in!

Why Renters Insurance Matters

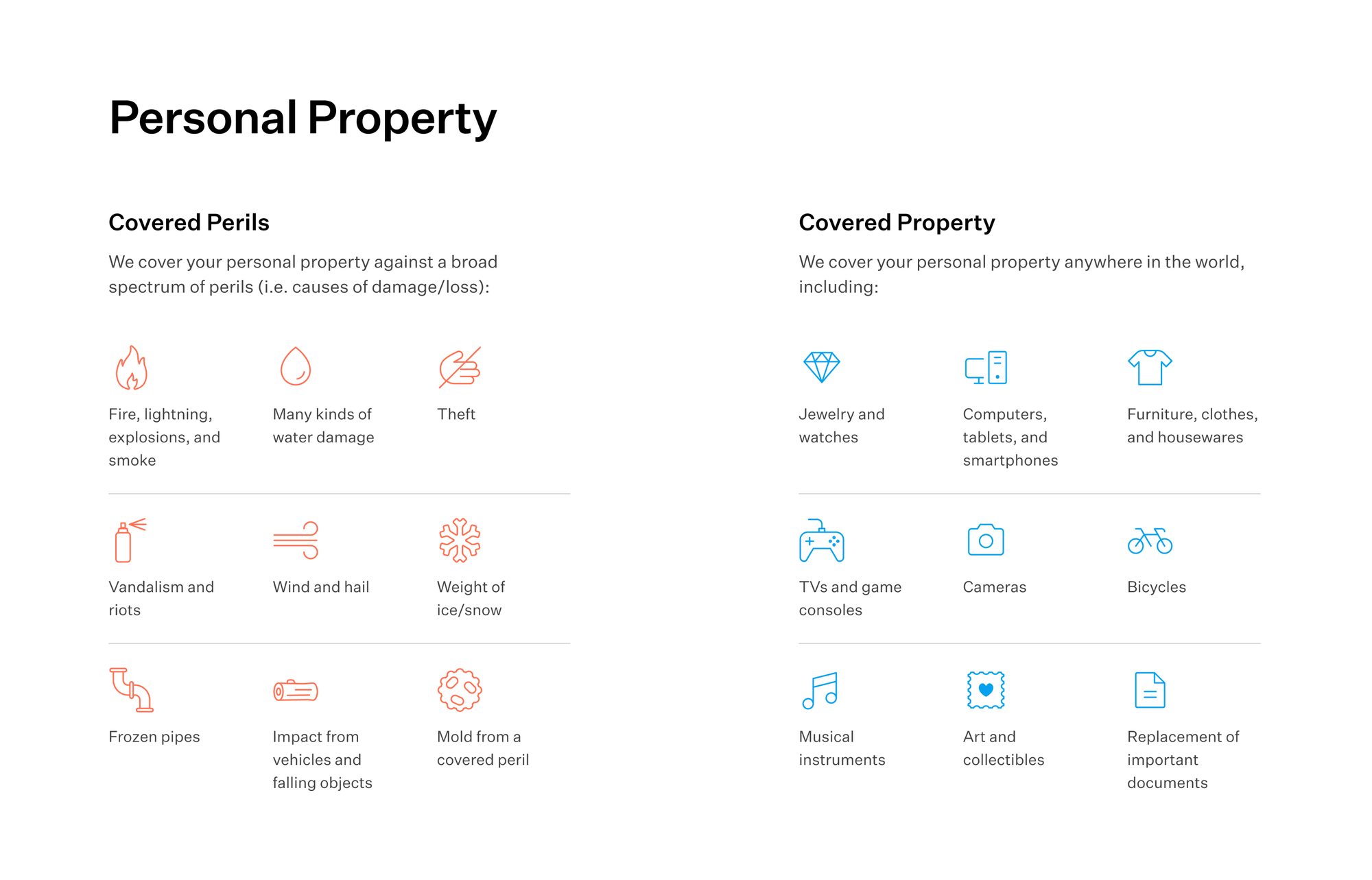

First things first, let's clear up a common misconception: renters insurance is not just for rich people with fancy stuff. It's for anyone who wants to protect their belongings and avoid financial setbacks if something goes wrong. In a nutshell, renters insurance offers:

- Personal Property Coverage: Your stuff – clothes, furniture, electronics – it's all protected from theft, fire, vandalism, and more.

- Liability Coverage: If someone is injured in your place or you accidentally cause damage to someone else's property (like if the fire started in your place and spread to your neighbor's place), this coverage has your back.

- Temporary Housing Coverage / Additional Living Expenses: If your place becomes unlivable due to a covered incident, this helps with additional expenses like hotel stays and meals.

At Goodcover, your roommates on the lease are automatically covered, simplifying the process and often saving you money, too. However, if someone prefers to have their own policy, they certainly can.

The Roommate Insurance Talk: How to Avoid Awkwardness

Talking about money can be awkward, but it's necessary to have an open and honest conversation about renters insurance with your roommates. Here are some icebreakers to get you started:

- "What are the most important things you'd want to replace if something like a fire happened in our place?"

- "How much do you think it would cost you to replace those things out of pocket?"

- "How much are we comfortable spending on insurance each month?"

- "Should we get a joint policy or individual ones?"

Pro tip: Discuss potential conflicts upfront. For example, what if one roommate has more valuable stuff that could increase your monthly premium? How will you handle disagreements about whether to file a claim? Addressing these issues early on can prevent major headaches later.

Finding the Right Policy: Tips for Comparison Shopping

Once everyone's on board, it's time to find the perfect policy. Consider these factors:

- Coverage Limits: How much will the policy pay out if your belongings are damaged or stolen? All Goodcover policies come with replacement cost coverage, meaning you'll get enough money to replace your items new (up to your coverage limits, of course).

- Deductible: This is the amount you'll pay out of pocket before the insurance kicks in. A lower deductible means your annual premium will be higher, while a higher deductible will lower your annual premium. Learn more about deductibles here.

Get quotes from multiple providers and find the best deal for your needs. At Goodcover, you can get a renter insurance quote faster than you can listen to your favorite song, and you can even bind your policy right from the comfiest spot on your couch – no agents, no big fuss. Just simple, modern insurance.

The Cost-Sharing Conundrum: 3 Fair Ways to Split the Bill

- The Equal Split: The simplest option is to divide the cost evenly among roommates. This works well if everyone has similar belongings and coverage needs.

- Pros: Easy, simple, straightforward.

- Cons: May not be fair if some roommates have significantly more valuable items.

- The Proportional Split: This method takes into account the value of each roommate's belongings. Those with more expensive items pay a larger share of the premium.

- Pros: More equitable in some cases.

- Cons: Can be tricky to determine the value of belongings, and some might feel uncomfortable disclosing this information.

- The Room Size/Usage Split: Here, the cost is split based on room size or how much each roommate uses shared spaces.

- Pros: Takes into account individual living situations.

- Cons: May not reflect the actual value of possessions.

Some roommates opt for a hybrid approach, combining elements of these methods. For instance, you could split the base cost equally and adjust for individual property values.

The best way to figure out what you'll pay is to get a free, instant Goodcover quote. Simply answer a few questions and see your pricing update in real-time.

Life Happens: Handling Changes and Adjustments

Roommate situations are rarely static. People move out, new people move in, and your belongings change over time. It's important to revisit your policy and cost-sharing agreement whenever there's a change. For example:

- New roommate: Discuss their coverage needs and adjust the cost-sharing arrangement accordingly.

- Big purchase: If someone buys a pricey item, consider adjusting the split to reflect the increased value of their belongings.

- Inflation: Prices go up, and inflation affects your renters insurance coverage. It's wise to review your policy annually to ensure your coverage limits are still adequate.

Put It in Writing: The Roommate Insurance Pact

To avoid misunderstandings and potential conflicts, put your cost-sharing agreement in writing. Include:

- How much each roommate pays.

- Payment deadlines.

- How you'll handle changes to the policy or cost-sharing arrangement.

Make sure every roommate entering the agreement signs and gets a copy.

The Bottom Line: Don't Wait for Disaster to Strike

Renters insurance is an important safeguard, and it doesn't have to be a source of stress for roommates. Have an open conversation, explore your options, and create a fair cost-sharing plan so you can enjoy peace of mind knowing you're all protected.

Don't wait for a disaster to strike – start the conversation and get insured today!

Note: This post is for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.